The global robotics industry has reached a paradoxical junction where technological sophistication has never been higher, yet the gap between experimental success and commercial scalability remains stubbornly wide. While the International Federation of Robotics (IFR) reports a record-breaking operational stock of 4.3 million industrial units as of 2023, the transition from controlled environments to the chaotic reality of public and industrial spaces is exposing a critical "reliability gap." This phenomenon, often referred to as the "99% problem," suggests that while achieving near-perfect performance is relatively swift, the final one percent of operational reliability—handling the infinite variety of real-world "edge cases"—represents the most significant barrier to the widespread adoption of autonomous systems.

The Statistical Landscape of Global Robotics

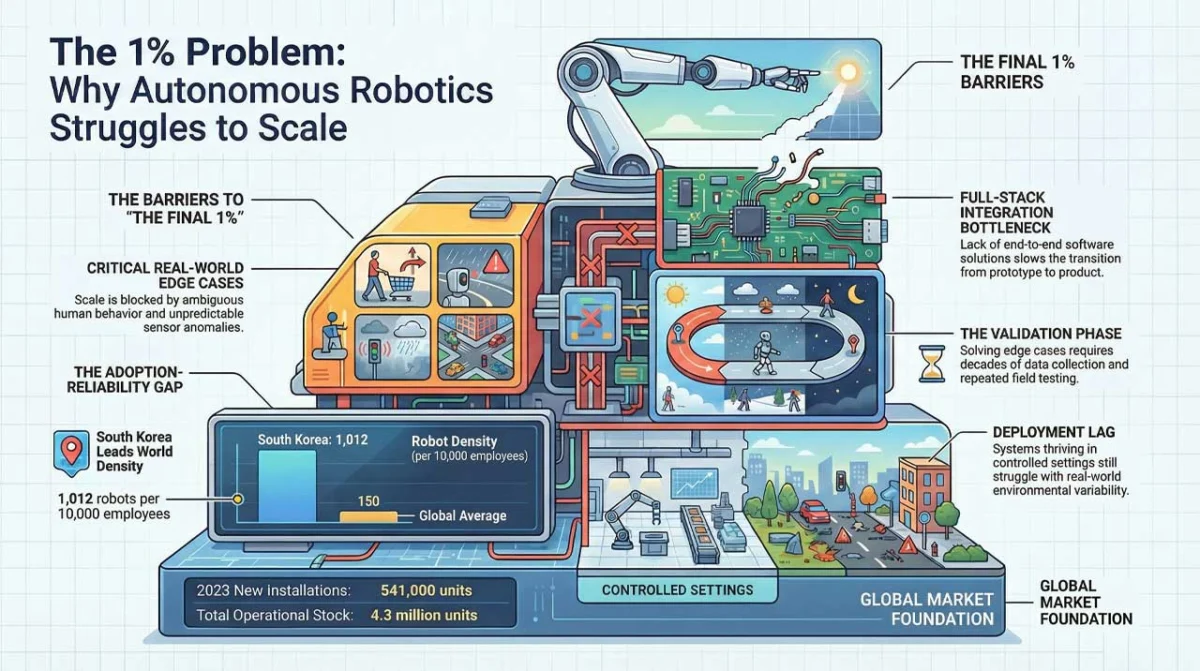

The current state of the industry is defined by massive growth in hardware deployment but significant friction in software autonomy. According to the World Robotics 2024 report by the IFR, 541,000 new industrial robots were installed globally in 2023 alone. This growth is driven by a convergence of labor shortages, rising wages, and the pursuit of operational efficiency.

South Korea stands at the vanguard of this movement. The nation currently holds the highest robot density in the world, with 1,012 robots per 10,000 employees—a figure ten times higher than the global average. This density is fueled by Korea’s dominance in electronics and automotive manufacturing. However, even in this highly automated environment, the majority of systems operate within "caged" or highly structured settings. The next frontier—autonomous mobile robots (AMRs) and service robots—is proving far more difficult to master than the fixed-arm predecessors of the previous decade.

Understanding the 99 Percent Problem

The concept of the "99% problem" highlights a structural mismatch in how autonomous systems are developed and deployed. In an interview regarding the state of the industry, Vivek Burhanpurkar, CEO of Cyberworks Robotics, noted that achieving high levels of safety and functionality in a lab or a mapped warehouse is straightforward. The challenge lies in the remaining one percent of scenarios that the system has never encountered before.

In the context of robotics, 99% reliability is actually a failure. If a robot performs 1,000 maneuvers a day—a low estimate for a commercial unit—a 1% failure rate means ten critical errors or "hallucinations" every single day. In environments like hospitals, airports, or high-traffic warehouses, ten interruptions per day render the technology economically unviable and potentially dangerous.

These "edge cases" include:

- Environmental Variability: Sudden changes in lighting, such as glare from glass facades or the strobe lights of emergency vehicles, which can "blind" optical sensors.

- Sensor Noise and Signal Interference: Reflections from polished floors or electromagnetic interference in industrial zones that disrupt LiDAR and ultrasonic sensors.

- Unpredictable Human Behavior: The erratic movements of children, pets, or distracted pedestrians in public spaces that do not follow the programmed logic of "standard" obstacles.

- Dynamic Obstacles: Objects that are partially transparent, like glass doors, or objects that change shape, such as hanging plastic curtains in cold-storage facilities.

The Evolution of Autonomy: A Chronology of Complexity

To understand why the industry is currently stalled at the "validation phase," it is necessary to look at the timeline of autonomous development:

- The Era of Pre-Programmed Automation (1960s–1990s): Robots operated on fixed paths with no "vision." They were safe only because they were physically separated from humans.

- The Introduction of Basic Perception (2000s–2010s): The integration of LiDAR and basic computer vision allowed robots to stop when they detected an obstacle. However, they lacked the "intelligence" to navigate around it or understand the context of the obstacle.

- The AI and Machine Learning Boom (2015–Present): Neural networks and Deep Learning significantly improved object recognition and path planning. Robots can now identify a "human" versus a "forklift."

- The Current Validation Bottleneck (2024 and Beyond): The industry has realized that better algorithms do not automatically result in better reliability. The focus has shifted from "Can the robot see?" to "Can the robot be trusted to operate without a human supervisor for 1,000 hours straight?"

South Korea’s Strategic Shift from Adoption to Validation

South Korea’s Ministry of Trade, Industry and Energy (MOTIE) has recognized that maintaining the country’s lead in robotics requires more than just high installation numbers; it requires a robust regulatory and safety framework. Historically, Korean robotics policy focused on hardware subsidies and R&D for core components like actuators and sensors.

However, recent policy shifts indicate a move toward "validation." The South Korean government has begun establishing "Regulatory Sandboxes" where autonomous robots can be tested in real-world urban environments under supervised conditions. This is a direct response to the realization that institutional frameworks and safety standards—such as those governing mobile robots on public sidewalks—remain incomplete.

For Korean Original Equipment Manufacturers (OEMs), the stakes are high. While companies like Hyundai (through Boston Dynamics) and Doosan Robotics are making strides, they face the same systemic friction identified by global experts. McKinsey & Company data suggests that timelines for fully autonomous systems have slipped by an average of 12 to 24 months across the board as the complexity of real-world integration becomes more apparent.

The Hidden Costs of Full-Stack Integration

A significant and often underestimated hurdle for startups and OEMs is the lack of "full-stack" software solutions. Many robotics companies develop impressive navigation modules or perception algorithms in isolation. However, a commercially viable product requires the seamless integration of:

- Fleet Management: Coordinating hundreds of robots without collisions or deadlocks.

- Cybersecurity: Protecting autonomous units from being hijacked or disabled.

- Maintenance Protocols: Predictive systems that identify hardware wear before it causes a "1%" failure.

- Interoperability: The ability for a robot from one manufacturer to communicate with elevators, doors, and robots from another manufacturer.

Without a full-stack approach, companies often face "integration debt," where they spend more time and money fixing the interactions between different software modules than they did building the original technology. This leads to high maintenance costs and slow deployment cycles, which can exhaust the capital of even well-funded startups.

Implications for Investors and Policymakers

The "99% problem" suggests a shift in how the robotics market will be evaluated in the coming years. Investors are moving away from companies that merely showcase "cool" demos in controlled settings toward those that can demonstrate long-term "Mean Time Between Interventions" (MTBI).

For policymakers, the challenge is to create safety standards that are stringent enough to protect the public but flexible enough to allow for the collection of the "edge case" data necessary for improvement. The "decades of time" mentioned by Vivek Burhanpurkar refers to the cumulative data required to train AI models on rare events. Without a way to safely expose robots to these rare events, the "1%" will never be solved.

Analysis: The Path Forward

The transition of autonomous robotics from "experimental" to "ubiquitous" depends on three key pillars:

First, Data Sharing and Standardization. The industry must move toward common standards for edge-case reporting. If every manufacturer keeps their failure data in a silo, the collective learning of the industry is slowed.

Second, Simulation vs. Reality. While digital twins and high-fidelity simulations are helpful, they cannot yet perfectly replicate the "noise" of the physical world. There is no substitute for physical "miles on the ground."

Third, The Human-in-the-Loop Transition. Rather than aiming for 100% autonomy immediately, the most successful companies are likely to be those that implement "remote teleoperation" as a bridge. When a robot hits an edge case it cannot solve, a human operator in a central hub takes control, solves the problem, and the data is used to train the system for the next time.

Conclusion: The Final Mile Defines the Market

The robotics industry is no longer in its infancy, but it is experiencing a difficult adolescence. The "99% problem" is a reminder that in the physical world, the laws of physics and the unpredictability of human environments are far more unforgiving than the digital realms of pure software.

For South Korea, the challenge is to leverage its high robot density to become the global testing ground for these final-mile solutions. The next phase of global competition will not be won by the company that builds the most "intelligent" robot, but by the one that builds the most reliable one. As the gap between technical capability and deployment readiness narrows, the "1%" will become the most valuable territory in the global tech economy. Those who can bridge this last mile will not just lead the market; they will define the future of human-robot interaction.