The Republic of Korea is currently witnessing a massive acceleration in its quest to become a global artificial intelligence powerhouse, supported by an unprecedented influx of capital, aggressive policy frameworks, and large-scale infrastructure development. However, beneath the surface of this rapid expansion, a significant recalibration is occurring within the startup community. As the initial "hype cycle" of generative AI matures, conversations among founders, venture capitalists, and policymakers are shifting away from pure technical capability toward a more fundamental and urgent question: which AI startups can transform rapid innovation into durable, revenue-generating businesses within an increasingly cost-sensitive and competitive global environment.

This transition marks a pivotal moment for the Korean "K-Startup" ecosystem. While the country has successfully established itself as a leader in hardware and high-speed infrastructure, the software and service-oriented AI sector is now facing a "trial by fire" regarding commercial sustainability. The focus is no longer merely on whether a team can build a sophisticated large language model (LLM) or a computer vision system, but whether that system solves a problem significant enough for customers to pay for it at a price that exceeds the rising costs of AI computation.

The Strategic Blueprint: Korea’s 2030 AI Vision

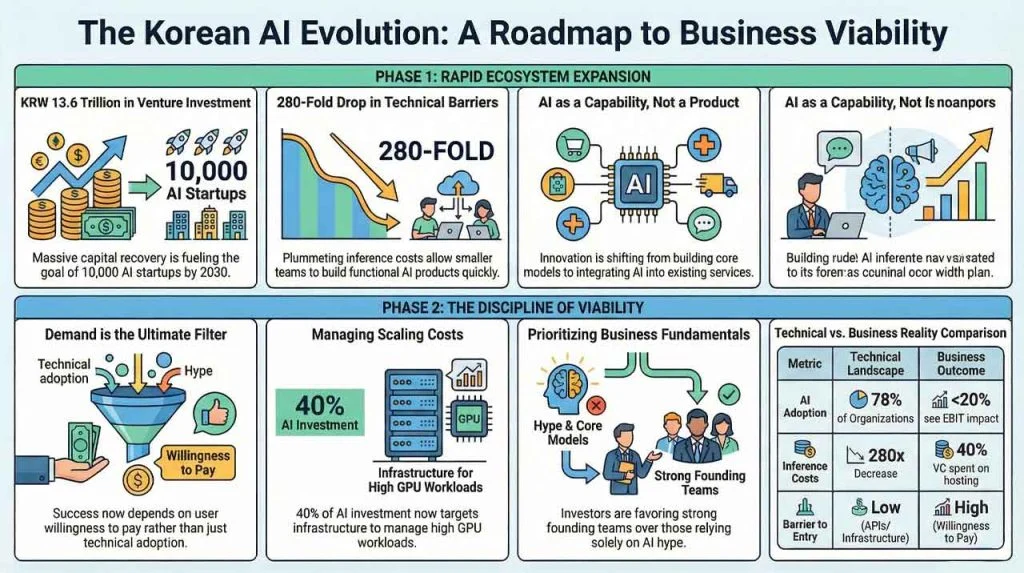

The current trajectory of the Korean AI market is largely dictated by the Ministry of SMEs and Startups (MSS), which has implemented a comprehensive long-term plan known as the K-Venture Blueprint 2030. This initiative is designed to foster 10,000 AI and deep-tech startups by the end of the decade, effectively positioning Korea as a central hub for the "Fourth Industrial Revolution." To support this ambitious goal, the government has facilitated a significant recovery in venture investment, which reached KRW 13.6 trillion in 2025. This capital injection signals a robust return of private and public confidence following the global economic cooling of previous years.

The government’s role extends beyond simple funding. By expanding access to high-performance computing (HPC) infrastructure and providing "R&D vouchers," the state is attempting to lower the barrier to entry for early-stage firms. However, this abundance of support has created a crowded marketplace. With thousands of new entities entering the fray, the differentiation between a "research project" and a "viable business" has become the primary metric for survival.

The Commoditization of Technical Innovation

One of the most significant drivers of this strategic shift is the rapidly falling cost of AI development. According to the Stanford AI Index 2025, the industry has seen a staggering 280-fold decrease in inference costs for models equivalent to GPT-3.5 between 2022 and 2024. Simultaneously, global AI adoption reached 78% of organizations by 2024. These statistics suggest that the "moat" of technical complexity is shrinking.

In the early stages of the AI boom, simply having the expertise to train a model was a competitive advantage. Today, the proliferation of open-source models, accessible APIs, and standardized cloud infrastructure means that small teams can assemble functional, high-performance AI products in weeks rather than years. In the Korean context, this has led to a surge in application-level startups that leverage existing foundational models to serve niche domestic industries, such as K-content, logistics, and specialized manufacturing.

However, as building AI becomes easier, the competitive landscape becomes more saturated. When the underlying technology becomes a commodity, the value of a startup shifts from its code to its market position, data proprietary, and customer relationships. This has forced Korean founders to look beyond the "AI" label and focus on the traditional fundamentals of business: unit economics, churn rates, and customer acquisition costs.

Demand as the Primary Filter for Survival

As technical barriers fall, consumer and enterprise demand has emerged as the ultimate filter for startup viability. Hojoung Lee, CEO of the AI-driven firm Undermilli, notes that the operational reality for modern startups is dictated by the user’s "willingness to pay." In the early phase of the AI explosion, many companies relied on "freemium" models or subsidized growth to capture market share. However, as investors demand paths to profitability, the focus has shifted to whether the AI provides a "must-have" value proposition rather than a "nice-to-have" novelty.

This sentiment is echoed by global data. A 2025 McKinsey report on the state of AI revealed a sobering reality: while adoption is at an all-time high, over 80% of organizations have yet to see a tangible impact on their earnings before interest and taxes (EBIT) specifically from generative AI. This "impact gap" suggests that while businesses are experimenting with AI, they are struggling to integrate it into their core value chains in a way that generates measurable profit. For Korean startups, this means that the sales cycle is becoming more rigorous; enterprise clients are no longer satisfied with a demo—they require proof of return on investment (ROI).

The Infrastructure Trap and the Economics of Scale

While the cost of starting an AI company has decreased, the cost of scaling one remains prohibitively high. This creates a structural paradox in the Korean ecosystem. The South Korean government is currently investing heavily in domestic GPU clusters and national AI compute centers to reduce reliance on foreign providers like NVIDIA and AWS. Despite these efforts, the sheer volume of data and processing power required for sophisticated AI services continues to strain the balance sheets of mid-sized startups.

OECD data from 2025 indicates that over 40% of all AI venture investment is currently being funneled into the infrastructure and hosting layers. This leaves application-level startups in a difficult position: they must compete for the remaining 60% of capital while paying a significant portion of their revenue back to the infrastructure providers. For a Korean startup to be viable, it must develop an "infrastructure-efficient" architecture. This has led to a trend of "Small Language Models" (SLMs) and "Edge AI," where processing is done locally or via smaller, more efficient models to preserve margins.

Investor Sentiment: Moving Beyond the "AI-Only" Narrative

The evolution of investor behavior is perhaps the most visible sign of the market’s maturation. Urska Vracun, an active angel investor in the early-stage ecosystem, suggests that the "AI" prefix is no longer enough to secure a premium valuation. Investors are returning to traditional evaluation criteria, with a heavy emphasis on the cohesion and experience of the founding team.

A notable shift in the investment community is the preference for "AI-enabled" businesses over "AI-only" businesses. Vracun points out that startups which do not base their entire value proposition on a single AI model are often viewed as more resilient. This is because they are less vulnerable to "platform risk"—the danger that a major player like OpenAI or Google will release a feature that renders the startup’s entire product obsolete overnight.

Furthermore, there is a growing concern regarding "narrative inflation." In 2023 and 2024, many Korean startups were able to raise funds based on the promise of AI integration. By 2025, the market has entered a period of "valuation correction," where companies are being judged on their actual revenue growth and the defensibility of their market niche. Investors are now looking for "boring" metrics: sustainable growth, high retention, and a clear path to becoming a "Unicorn" (a startup valued at over $1 billion) based on cash flow rather than hype.

Chronology of Korea’s AI Evolution

To understand the current state of the market, it is essential to look at the timeline of events that brought Korea to this juncture:

- 2022: The Awakening. The global release of ChatGPT triggers a surge in interest across the Korean peninsula. The government announces the first phase of the AI National Strategy.

- 2023: The Proliferation. Hundreds of Korean startups pivot to generative AI. "K-LLMs" like Naver’s HyperCLOVA X emerge, providing a localized foundation for domestic developers.

- 2024: The Infrastructure Push. Realizing the high cost of compute, the Ministry of Science and ICT begins subsidizing GPU access. The "K-Venture Blueprint 2030" is officially launched.

- 2025: The Great Recalibration. Venture capital reaches KRW 13.6 trillion, but the criteria for funding become significantly stricter. The focus shifts from "capability" to "viability."

Implications for Global Operators and Founders

The shift occurring in South Korea serves as a bellwether for the global AI industry. For international startup operators and investors looking at the Korean market, three practical implications are now clear.

First, real demand is the new baseline. The era of "build it and they will come" is over. Startups entering the Korean market must demonstrate a deep understanding of local industry pain points, particularly in sectors like elderly care, semiconductor logistics, and cybersecurity, where AI can provide immediate, billable value.

Second, cost discipline is the ultimate determinant of survivability. Founders who cannot manage their "compute burn" will find it impossible to scale, regardless of how much venture capital they raise. The ability to optimize model performance and leverage hybrid cloud/on-premise solutions is becoming a core competency.

Third, AI must be viewed as an enabler, not a standalone business. The most successful Korean startups in the coming years will likely be those that integrate AI into existing workflows to make them 10x more efficient, rather than trying to create entirely new "AI-first" categories that require massive shifts in user behavior.

Conclusion: From Innovation to Discipline

The South Korean AI ecosystem is not experiencing a slowdown, but rather a sophisticated evolution. The transition from a focus on technical innovation to business discipline is a sign of a maturing market. While the government continues to provide a safety net of infrastructure and funding, the responsibility has shifted to the founders to prove that their innovations can survive in a cold, market-driven reality.

The next phase of Korea’s AI journey will not be defined by the number of parameters in a model or the speed of a chip. It will be defined by the resilience of its entrepreneurs and their ability to build sustainable companies that contribute to the national economy. As the "K-Venture Blueprint 2030" moves forward, the winners will be those who recognize that while AI is the engine of the future, business fundamentals remain the steering wheel. The global community will be watching closely as Korea attempts to balance this high-speed growth with the rigorous discipline required to build a truly durable AI powerhouse.